Simple, Cost-Effective Solutions

Helping organisations

for over 20 years

For simple, cost-effective and accurate payroll solutions, choose Legislator™ software from CPS – an innovative, automated cloud-based system that is accessible from any location. It is guaranteed to save you time, increase accuracy and cut costs.

Your Trusted UK Payroll Provider

Our payroll software is versatile enough to cater to any business type, from fresh start-ups to established organisations. We’re committed to going the extra mile to grasp your unique needs.

Cut down on time and expenses with our straightforward, quick, and hassle-free bespoke payroll software solutions from CPS.

Known for our reliability and precision, we’re dedicated to providing a risk-free payroll services solution that aligns with your outsourcing requirements.

You have the flexibility to use our cutting-edge, industry-leading, cloud-based payroll software as a standalone product, or you can choose our bureau service or a fully outsourced payroll services package for a completely managed service

Why Should Payroll Services Be Outsourced?

Managing payroll in-house can turn into a complicated and time-consuming chore in the business world.

Opting for outsourcing payroll services is a smart move, offering a range of advantages that can greatly enhance the efficiency and security of your business operations.

Managed payroll solutions provide a streamlined approach to handling this essential task.

- Time-Saving: By using payroll accounts software, you can avoid spending hours on calculating pay, taxes, and handling paperwork, allowing you to concentrate on core business activities.

- Cost-Effective: It eliminates the need for in-house payroll staff, reduces the costs associated with payroll systems software, and minimises the risk of costly errors or tax compliance issues.

- Access to Expertise: We specialise in our field and constantly update our knowledge in line with current laws and regulations. This expertise means less risk of errors and non-compliance with tax laws.

- Enhanced Security: Payroll processing involves sensitive employee data. Professional payroll services often have robust security measures in place to protect against data breaches, fraud, and other risks.

- Regulatory Compliance: Keeping up with the ever-changing payroll regulations and tax laws is a challenge. Outsourcing payroll services ensures that your business stays compliant.

Why is Outsourcing Good for Small Companies and Businesses?

Small businesses often find themselves grappling with the intricacies of payroll. With fewer resources and specialised knowledge, handling payroll in-house can turn into a lengthy and expensive process.

This is where the role of outsourcing payroll services becomes crucial, providing a host of advantages tailored to streamline this vital business function. Utilising payroll software for small businesses can further simplify and enhance this process.

- Cost-Effective Solution: Outsourcing payroll services offers a simple, cost-effective solution for small and medium-sized businesses, freeing up valuable in-house resources and staff.

- Avoids the Hassle of In-House Management: Managing payroll in-house involves recruiting, training, and managing staff, as well as purchasing and managing software. This can be costly and adds worry and risk to the business.

- Overcomes Limited Resources: Many small businesses can’t afford to hire experienced payroll staff or have a dedicated account manager, leading to reliance on unqualified admin staff. This can result in longer processing times and potential errors.

- Addresses Software and Security Issues: Small businesses often can’t afford top-tier payroll software solutions and may resort to insecure methods like email or paper for payroll information, increasing security risks.

- Online Solutions for Efficiency: Our online payroll services are designed to streamline the payroll process, easing the administrative burden and making life easier for employees.

Why Choose CPS?

As a UK-based outsourced payroll services provider, CPS has been supporting businesses of all types and sizes for over 20 years. Our focus is on delivering highly customised, fast, efficient, and stand-alone payroll solutions.

- Long-Standing Experience: We’ve been assisting a diverse range of businesses with their payroll needs for over two decades.

- Tailored Payroll Solutions: Our payroll services are not just efficient and fast; they are also highly customised to meet the unique needs of each business we work with.

- Commitment to Personal Service: We invest significant time in understanding every detail of your requirements, ensuring the service we provide is a perfect match for your needs.

Payroll Solutions

Providing simple and cost-effective outsourced UK payroll services to give you full control.

Payroll Software

Intuitive, highly secure and cloud-based payroll software accessible from any location, guaranteed to save you time, increase accuracy and cut costs.

HR Software

Our cloud-based HR payroll software, Legislator™, is incredibly user-friendly and one of the most potent tools crafted to simplify HR administration tasks.

Managed Services

Our managed payroll solutions are dedicated to guaranteeing that your payroll is exceptionally precise, consistently using the correct tax codes, always in line with the latest legal requirements, and risk-free.

Pension Enrolment

Our Pension Auto-Enrolment Software is designed to take care of the entire burden ensuring you meet your legislative obligations with the minimum of effort.

Frequently Asked Questions

With over 20 years of experience, we are one of the most versatile payroll service providers in the UK.

From all of the UK payroll services providers out there, why is your business different?

So let us get right to the point. We focus on delivering services of exceptionally high quality. If you choose to work with us, you’ll get:

- The confidence that your company’s payroll will consistently be run accurately and delivered on time, every time.

- Highly qualified and CIPP accredited experts, giving you the reassurance that you can focus on doing what you do best while all aspects of your payroll are being taken care of.

- A dedicated account manager who you can always contact for help whenever you need it.

- Full customer support from our pragmatic (and jargon free!) specialists, making sure that your experience of outsourcing your payroll is as hassle free as possible.

No matter where you are in the world, as long as you have internet access, you’ll always have full access to your payroll information. All of the services we offer are cloud-based, available 24/7 every day of the year.

Is outsourcing payroll cost-effective?

Outsourcing also helps avoid the financial risks of errors and penalties due to non-compliance with tax laws and regulations. By delegating payroll to specialised providers, businesses can allocate their resources and focus more effectively on their core operations.

When should you outsource payroll?

- Business Growth: As your business grows, the complexity of payroll increases. Outsourcing can handle this complexity more efficiently.

- Time Constraints: If managing payroll in-house is consuming a significant amount of time that could be better spent on core business activities.

- Lack of Expertise: If your business lacks the expertise to manage payroll effectively and stay compliant with the latest tax laws and regulations.

- Cost Concerns: When the cost of managing payroll in-house (including staff, software, and potential penalties for errors) becomes too high.

Security and Privacy Concerns: If you’re concerned about the security of sensitive payroll data and want to ensure it’s managed with the highest level of security and compliance.

Give us one main reason why we should choose CPS and not another payroll company

We have a range of skills within the team that covers a wide range of sectors. Collectively there is highly specialised knowledge which means we are able to handle even the most complicated of payroll scenarios.

Our team is comfortable handling complex shift calculations, benefit allowances, holiday accruals, tax calculations, expense reimbursements, pension auto enrolment assessments… and all manner of other payroll related activities that your company might potentially require.

Sometimes with payroll companies, there are hidden charges. What’s the case with CPS?

We know it’s really important to ensure you are clear about exactly what you are getting for your money. We set out the agreement with a defined set of service levels so you can make sure you are happy with the service you will be receiving.

We charge for our online payroll services on an all-inclusive cost per payslip basis. This makes sure that you will know exactly what to expect here and now, and it also means that you will be aware of the future costs of our outsourcing payroll service if your company grows and your payroll requirements evolve as a result.

Does your company provide payroll solutions for sectors that require special assistance?

Here at CPS, we have a dedicated team of specialists who have specific experience of working with companies in sectors likely to have these more complex requirements: for example, finance, nursing homes, leisure, schools and other academic organisations, charities and even recruitment companies.

We are yet to come across an organisation where we are unable to accommodate their requirements! So no matter what sector your company operates in, contact us today for a discussion about what you need and for a free payroll services outsourcing quote.

What are the main benefits of using CPS compared to other companies?

When you use CPS, it becomes our responsibility to stay up to date with the fast-changing regulations, practices and methods – not yours. By outsourcing your requirements to our company, you have the reassurance of knowing your payroll is being taken care of by dedicated experts so you can concentrate on other priorities instead.

Another key benefit of using our professional fully managed payroll services is the fact that you have a year-round cover. With an in-house team, you always have the risk of someone going off sick and causing disruption to your payroll processes. Even planned leave can end up causing cover headaches – but by outsourcing your requirements, you don’t need to worry about any of this.

Finally, with our services, you don’t ever have to think about investing in new software or taking any form of action to ensure your software is kept up to date and fully compliant with the latest regulations. We take care of all of that for you.

What makes CPS more reliable & trustworthy than other payroll companies?

We pride ourselves on not having a ‘faceless’ call centre approach – we value the strength of the relationships we have. Our careful step-by-step approach helps us to start building the foundations of those relationships straight away. Right after the enrolment phase, we assign you a dedicated account manager ready to answer any questions you might have. They know your name, your business details and understand the specifics of your company’s needs. This all helps you avoid time-consuming ticket systems, telephone queues, and lengthy email exchanges when you need our help.

Some of the comments that we have had about the team are that they have “consistently been brilliant” and that we have very open and honest relationships with our clients. If there is an issue or query, we deal with it quickly. Some of our clients have been with us for over 20 years now which we think is a testament to the reliability and trustworthiness of the personal service we provide.

“Our CPS contact is doing such an amazing job for us, I just wanted to let you know how much we appreciate her. She is so unbelievably helpful. She has been a calm voice of reason and sanity in this time of fast changing rules and has been so professional and approachable all the way through (as always). Nothing is ever too much trouble and she does everything really quickly and efficiently. I really appreciate the help that she has given us and just wanted to recognise it. She is an absolute asset to your organisation.”

How much do your services cost?

Instead, we carefully assess your exact payroll requirements to determine the cost; to calculate the right price, we require specific sets of information such as the number of weekly/fortnightly/4-weekly paid staff, P11D, Pensions Automatic Enrolment support, and any other services that might be required over and above the basic payroll system.

How secure is my data with your organisation?

It goes without saying that handling and dealing with payroll systems software requires processing vast amounts of sensitive information in relation to your employees: names, social security numbers, bank details, addresses, salary information and so on. From GDPR through to physical and digital security, our exceptionally high standards ensure that your data is dealt with safely and securely, protecting you and your company from data loss, leakage, and misuse. All information is safely hosted in specialist UK data centres, which are operated by market leaders in the sector. Additionally, our core systems are replicated to multiple servers, monitored 24/7 and backed up every day.

As a company, we continue to invest in research and development, ensuring that all of our payroll company products are Cyber Essentials & Automatic enrolment certified and tested and approved by HMRC.

For companies looking for a personal touch, how customisable are CPS’s services?

At the same time, CPS’s dedicated payroll services team is always on standby and ready to advise on UK employment law.

What’s the smallest business size that CPS will work with?

While our unique software can deliver highly customisable payroll services for small businesses that can be tailored to suit any customer requests from the simplest to the most complex needs, we do focus on providing payroll solutions and services to medium and large businesses.

How suitable is CPS for very large businesses looking for corporate payroll services?

While CPS’s services might not be the cheapest in relation to some providers, the quality, simplicity, and effectiveness of these services compared to others makes sure that CPS continues to be one of the most in-demand payroll services providers in the UK. Large companies choosing CPS will benefit from regular face-to-face meetings at the firm’s offices and direct access to a dedicated account manager via email, zoom, and over the phone.

Will internal IT and payroll departments need to perform any structural changes to use CPS's services?

What makes CPS’s customer service stand out from the competition?

If you are looking for expert payroll services with a personal touch, CPS is the ultimate UK-based payroll service provider for you.

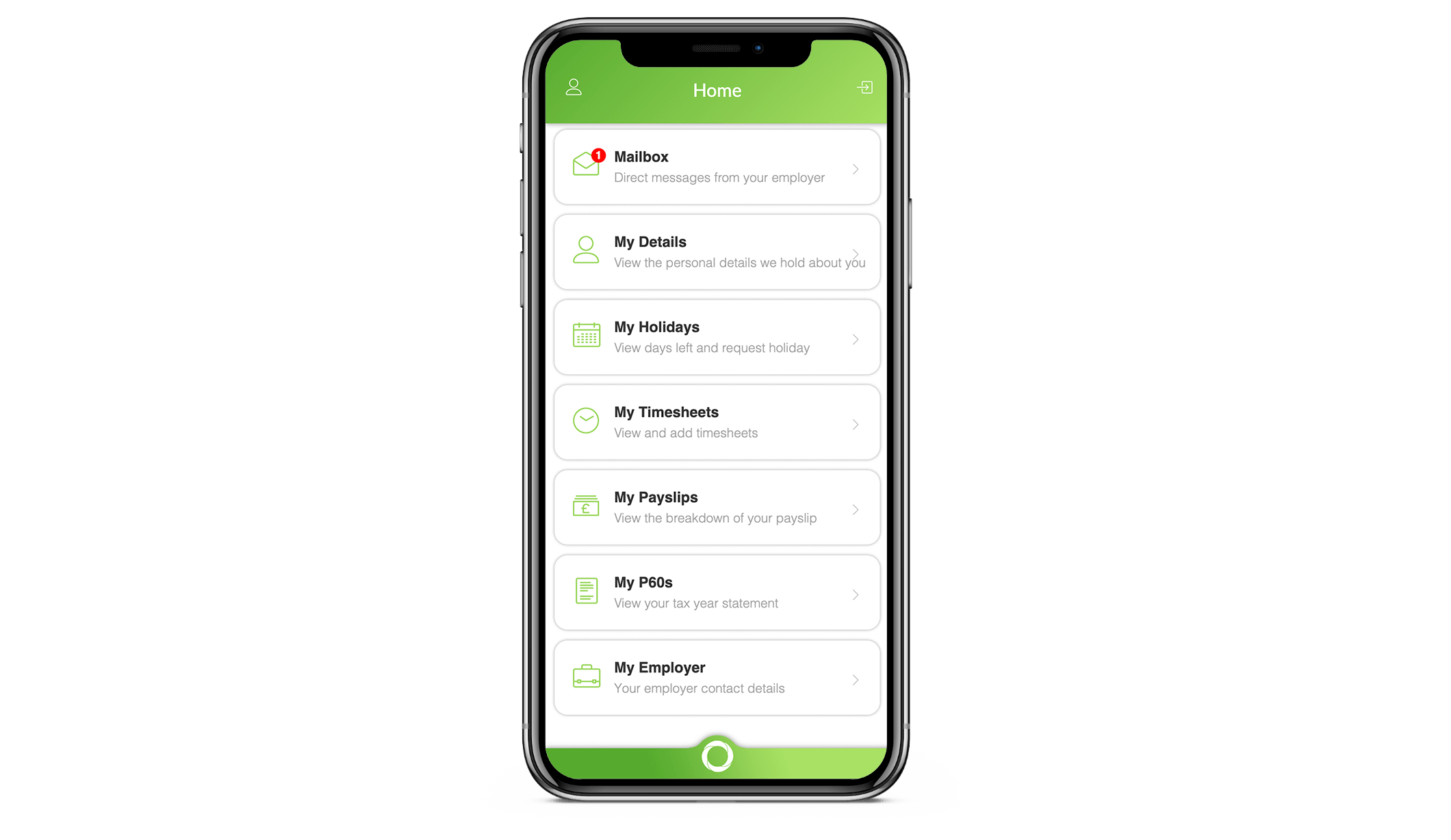

Mobile Apps For Your Employees

We continually invest in research & development to ensure that our payroll solutions continue to be amongst the very best on the market.

Helping Companies With Custom Payroll Solutions & HR Services

Highly customised, fast, stand-alone services designed to work with any type of business.

Smooth Transitions

We guarantee a smooth transition to our payroll services in a short timeframe so you can be sure that your workforce will be paid on time, even if they are paid weekly.

Risk Free Management

We continually invest in research and development to ensure that our payroll outsourcing solutions are up to date, easy to use and secure.

CIPP Qualified

Our friendly support staff are qualified by the Chartered Institute of Payroll Professionals and offer a fantastic level of customer service. We believe in good communication.

Fast Turnaround

Most payroll companies take 7-10 days to input & process payroll but we can do it in less than 3 days and late changes can be made up until the BACS file is transmitted.

CPS Accreditations

Trusted by all the key bodies in the UK

See How We Can Help You

CPS has become the outsourced provider of choice for many businesses across the UK. So if you are looking for payroll providers or HR solutions for your company, why not get in touch to discuss your needs with one of our friendly advisors to see how CPS can help you? We’d be delighted to give you an online demonstration of the software, provide you with a quote and answer all the questions you have.